Cherisha Chapman, Steve Niehoff, and Pete Swisher | February 3rd, 2023

Startup Tax Credits under SECURE 2.0—Easy Reading Version with FAQs

The enhanced startup credit is possibly the single highest impact provision of SECURE 2.0 and is worth studying in its actual, statutory form.

The actual language of the SECURE 2.01 provisions on startup tax credits is below, but merged with the old law, cross-referenced, and formatted for easy reading. We follow it with answers to some frequently asked questions (FAQs) and a diagram for helping determine whether an employer is eligible for the credit.

In the first few weeks since SECURE 2.0 became law, we have seen contradictory interpretations of the new startup credits within the pension community. In such an environment, the best way to understand the new rules is to read them yourself. We have endeavored to make it easy for you to do so.

“Back of the Napkin” Summary for Financial Professionals

The basic question for financial professionals is “how much credit is available” for employers who start a new plan? Is it enough to make starting a plan financially viable? This piece is designed to help financial professionals get comfortable answering that question.

For the majority of businesses, those with 50 or fewer employees, the available credit is:

• Basic credit: $250 x eligible NHCEs up to $5,000 (minimum credit $500)

• Employer contribution credit: 100%-100%-75%-50%-25% of employer contributions in years 1-2-3-4-5 up to a max of $1,000 per employee, but only for employees making $100,000 or less

• Additional $500 for including auto-enrollment (which is mandatory anyway starting in 2025, subject to certain exceptions)

Executive Summary

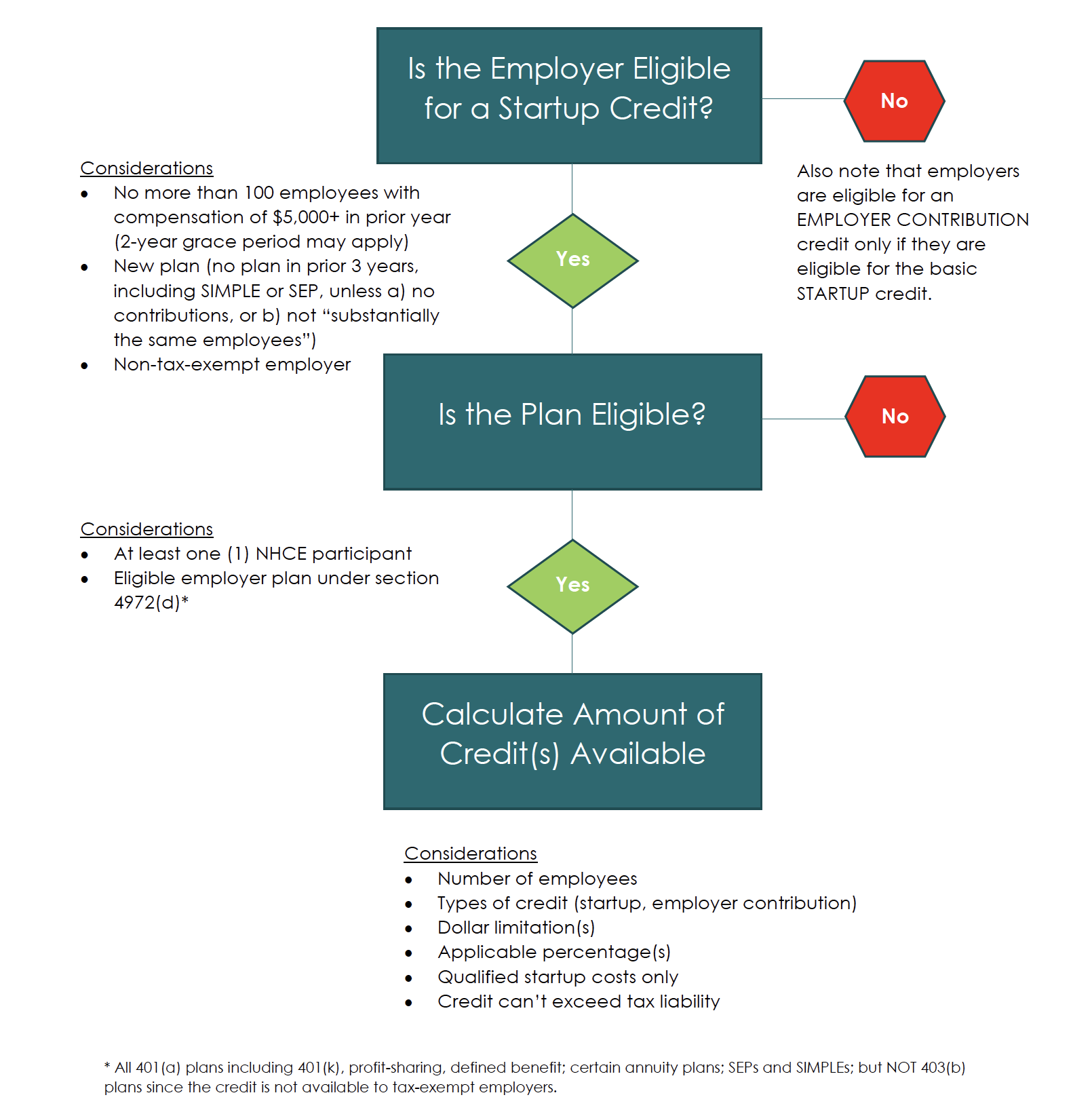

- First step: determine if the employer is eligible for the credit using the Eligibility Flowchart supplemented by checking the actual text of the law. Key points:

-

- 100 or fewer employees with $5,000+ compensation in the prior year

- 2-year grace period may apply if the employer qualifies in year one but subsequently grows beyond the 100-employee level

- Employer must be non-tax-exempt

- The plan must be a “new” plan (i.e., there is no “old” plan for the prior three years), and this is less straightforward than it sounds because the definition is complicated and there are threshold circumstances that will routinely arise to confound financial professionals, such as:

- Employer has a SIMPLE or SEP IRA and wants to “upgrade” to a stand-alone 401(k) or PEP—in general, no credit is available UNLESS

• Covered employee population changes substantially (e.g., a lot more people get covered)

• There were no contributions to the old plan for three years

-

-

-

- A merger or acquisition transaction is involved (in general, if there was a plan before the transaction, the safe course is to assume the credit is unavailable, but the actual rules are more complicated and require professional tax advice beyond the scope of this article)

- Employer crosses the 100-employee threshold during the years the credit is claimed, which triggers different treatment for purposes of the basic startup credit versus the employer contribution credit (i.e., the 2-year grace period is different for one versus the other)

- Second step: determine if the plan is eligible. The types of new plan the employer must start (and cannot already have, or else the plan is not “new”) to claim the credit are:

-

- 401(a): primarily profit-sharing, 401(k), defined benefit

- SIMPLE IRA

- SEP IRA

- NOT 403(b) or governmental

In addition, there must be at least one eligible non-highly compensated employee (NHCE).

-

-

-

Third step: calculate the credit

- Basic startup credit

-

- For 50 or fewer employees: $250 x eligible NHCEs, up to $5,000 (minimum credit $500), plus $500 auto-enrollment credit, if applicable

- For 51-100 employees: 50% of ($250 x eligible employees), still up to $5,000, plus $500 auto-enrollment credit, if applicable

- Credit is an offset against “qualified startup costs” for setup, administration, or employee retirement education costs; can include advisor/consultant, recordkeeping, TPA, and even settlor fees

- Employer contribution credit (for match/nonelective contributions)

- Actual contribution amount per employee up to $1,000 (but no credit for employees making more than $100,000) multiplied by the “applicable percentage”

- This amount applies up to and including 50 employees

- Reduce by 2% per employee over 50

- The “applicable percentage” is a declining percentage: 100% in years 1 and 2, 75% in year 3, etc. No credit after year 5.

- “Year 1” for this credit may be different than for the basic startup credit: year 1 for the basic startup credit can be the year before or the year of plan establishment; for the contribution credit year 1 is the year of establishment (which makes sense since there might be startup costs in the year before establishment but no employer contributions until the plan is live).

• Financial Professionals should be sure to use the words, “Check with your accountant or tax advisor.”

• Effective date as written in SECURE 2.0 Act Section 102(d): “The amendments made by this section shall apply to taxable years beginning after December 31, 2022.”

- Actual contribution amount per employee up to $1,000 (but no credit for employees making more than $100,000) multiplied by the “applicable percentage”

-

Steps to Calculate Eligibility for Credit

Updated Text of IRC Section 45E

Disclaimer: this is a best-efforts attempt to assemble the new law into readable form. We have adjusted punctuation and added explanations [in brackets] but otherwise attempted to produce the exact wording and numbering of the amended law.

IRC Section 45E2, as amended by SECURE 2.0 Section 102:

(a) General rule.

For purposes of section 383 in the case of an eligible employer, the small employer pension plan startup cost credit determined under this section for any taxable year is an amount equal to 50 percent of the qualified startup costs paid or incurred by the taxpayer during the taxable year.

(b) Dollar limitation.

The amount of the credit determined under this section for any taxable year shall not exceed—

(1) for the first credit year and each of the 2 taxable years immediately following the first credit year, the greater of—

(A) $500, or

(B) the lesser of—

(i) $250 for each employee of the eligible employer who is not a highly compensated employee (as defined in section 414(q)) and who is eligible to participate in the eligible employer plan maintained by the eligible employer, or

(ii) $5,000, and

(2) zero for any other taxable year.

(c) Eligible employer.

For purposes of this section—

(1) In general. The term “eligible employer” has the meaning given such term by section 408(p)(2)(C)(i).

[which section reads as follows:

“(I) In general

The term “eligible employer” means, with respect to any year, an employer which had no more than 100 employees who received at least $5,000 of compensation from the employer for the preceding year.

(II) 2-year grace period

An eligible employer who establishes and maintains a plan under this subsection for 1 or more years and who fails to be an eligible employer for any subsequent year shall be treated as an eligible employer for the 2 years following the last year the employer was an eligible employer. If such failure is due to any acquisition, disposition, or similar transaction involving an eligible employer, the preceding sentence shall not apply.”]

(2) Requirement for new qualified employer plans. Such term shall not include an employer if, during the 3-taxable year period immediately preceding the 1st taxable year for which the credit under this section is otherwise allowable for a qualified employer plan of the employer, the employer or any member of any controlled group including the employer (or any predecessor of either) established or maintained a qualified employer plan with respect to which contributions were made, or benefits were accrued, for substantially the same employees as are in the qualified employer plan.

(d) Other definitions.

For purposes of this section—

(1) Qualified startup costs

(A) In general. The term “qualified startup costs” means any ordinary and necessary expenses of an eligible employer which are paid or incurred in connection with—

(i) the establishment or administration of an eligible employer plan, or

(ii) the retirement-related education of employees with respect to such plan.

(B) Plan must have at least 1 participant. Such term shall not include any expense in connection with a plan that does not have at least 1 employee eligible to participate who is not a highly compensated employee.

(2) Eligible employer plan. The term “eligible employer plan” means a qualified employer plan4 within the meaning of section 4972(d).

[which section reads as follows:

(A) In general. The term “qualified employer plan” means—

(i) any plan meeting the requirements of section 401(a) which includes a trust exempt from tax under section 501(a),

(ii) an annuity plan described in section 403(a)5,

(iii) any simplified employee pension (within the meaning of section 408(k)), and

(iv) any simple retirement account (within the meaning of section 408(p)).

{i.e., all 401(a)6 plans including 401(k), profit-sharing, money purchase, target benefit, defined benefit; 401(a) plans funded solely by annuities; SEP and SIMPLE IRAs; NOT 403(b) plans, which makes sense since those employers pay no taxes and thus have no access to the tax credit}

(B) Exemption for governmental and tax exempt plans

The term “qualified employer plan” does not include a plan described in subparagraph (A) or (B) of section 4980(c)(1).

[which sections read as follows:

“(A) a plan maintained by an employer if such employer has, at all times, been exempt from tax under subtitle A, or

(B) a governmental plan (within the meaning of section 414(d))…”]]

(3) First credit year. The term “first credit year” means—

(A) the taxable year which includes the date that the eligible employer plan to which such costs relate becomes effective, or

(B) at the election of the eligible employer, the taxable year preceding the taxable year referred to in subparagraph (A).

(e) Special rules.

For purposes of this section—

(1) Aggregation rules. All persons treated as a single employer under subsection (a) or (b) of section 52, or subsection (m) or (o) of section 414, shall be treated as one person. All eligible employer plans shall be treated as 1 eligible employer plan.

(2) DISALLOWANCE OF DEDUCTION7. No deduction shall be allowed—

(A) for that portion of the qualified startup costs paid or incurred for the taxable year which is equal to so much of the portion of the credit determined under subsection (a) as is properly allocable to such costs, and

(B) for that portion of the employer contributions by the employer for the taxable year which is equal to so much of the credit increase determined under subsection (f) as is properly allocable to such contributions.

(3) Election not to claim credit. This section shall not apply to a taxpayer for any taxable year if such taxpayer elects to have this section not apply for such taxable year.

(4) Increased credit for certain small EMPLOYERS. In the case of an employer which would be an eligible employer under subsection (c) if section 408(p)(2)(C)(i) was applied by substituting ‘50 employees’ for ‘100 employees’, subsection (a) shall be applied by substituting ‘100 percent’ for ’50 percent’.

(f) Additional Credit for Employer Contributions by Certain Eligible Employers.

(1) IN GENERAL.—In the case of an eligible employer, the credit allowed for the taxable year under subsection (a) (determined without regard to this subsection) shall be increased by an amount equal to the applicable percentage of employer contributions (other than any elective deferrals (as defined in section 402(g)(3)) by the employer to an eligible employer plan (other than a defined benefit plan (as defined in section 414(j))).

(2) Limitations.—

(A) DOLLAR LIMITATION.—The amount determined under paragraph (1) (before the application of subparagraph (B)) with respect to any employee of the employer shall not exceed $1,000.

(B) CREDIT PHASE-IN.—In the case of any eligible employer which had for the preceding taxable year more than 50 employees, the amount determined under paragraph (1) (without regard to this subparagraph) shall be reduced by an amount equal to the product of—

(i) the amount otherwise so determined under paragraph (1), multiplied by

(ii) a percentage equal to 2 percentage points for each employee of the employer for the preceding taxable year in excess of 50 employees.

(C) Wage limitation.—

(i) IN GENERAL.—No contributions with respect to any employee who receives wages from the employer for the taxable year in excess of $100,000 may be taken into account for such taxable year under subparagraph (A).

(ii) WAGES.—For purposes of the preceding sentence, the term “wages” has the meaning given such term by section 3121(a).

(iii) INFLATION ADJUSTMENT.—In the case of any taxable year beginning in a calendar year after 2023, the $100,000 amount under clause (i) shall be increased by an amount equal to—

(I) such dollar amount, multiplied by

(II) the cost-of-living adjustment determined under section 1(f)(3) for the calendar year in which the taxable year begins, determined by substituting “calendar year 2007” for “calendar year 2016” in subparagraph (A)(ii) thereof.

If any amount as adjusted under this clause is not a multiple of $5,000, such amount shall be rounded to the next lowest multiple of $5,000.

(3) APPLICABLE PERCENTAGE. For purposes of this section, the applicable percentage for the taxable year during which the eligible employer plan is established with respect to the eligible employer shall be 100 percent, and for taxable years thereafter shall be determined under the following table:

|

In the case of the following taxable year beginning after the taxable year during which plan is established with respect to the eligible employer: |

The applicable percentage shall be: |

|

1st |

100% |

|

2nd |

75% |

|

3rd |

50% |

|

4th |

25% |

|

Any year thereafter |

0% |

(4) Determination of eligible employer; NUMBER OF EMPLOYEES. For purposes of this subsection, whether an employer is an eligible employer and the number of employees of an employer shall be determined under the rules of subsection (c)9, except that paragraph (2) thereof10 shall only apply to the taxable year during which the eligible employer plan to which this section applies is established with respect to the eligible employer.11

Notes from Prior IRS Guidance

The startup tax credit has existed for many years and was updated by SECURE 1.0, so we have IRS Form 8881and its instructions as guidance for how the IRS viewed the calculation previously, plus a plain language summary on the IRS website.

Click here for the Form 8881 Instructions.

Click here for the IRS summary of the credit.

NAPA Q&A

See the Q&A provided by the National Association of Plan Advisors (NAPA). Q&A provided by the National Association of Plan Advisors (NAPA) with respect to the prior rules under SECURE 1.0. Most of the questions and answers are still pertinent and accurate.

Which Employees Count Toward the Credit?

Some commentators have suggested that the employees to be counted for purposes of determining the credit amount are only those employees making $5,000 or more, but the text of the law and the IRS Form 8881do not appear to support that interpretation. From the amended statute, the employee count for determining the credit amount includes:

“…each employee of the eligible employer who is not a highly compensated employee (as defined in section 414(q)) and who is eligible to participate in the eligible employer plan maintained by the eligible employer…” (IRC Section 45E(b)(1)(B)(i), as amended by Section 102 of SECURE 2.0)

Who Decides Whether an Employer Qualifies for the Tax Credit?

It’s a tax credit: like any other deduction or credit, an employer decides whether to claim it via their tax return, with or without the help of tax advisors. The IRS can always disagree.

The “New Plan” Requirement and How it Interacts with SIMPLE and SEP IRAs

To qualify for the startup credit the plan must be “new” (i.e., a “startup”). “New” has a specific definition that is important to understand, since it eliminates the ability for most—but not all—sponsors of SIMPLE or SEP IRAs, as well as all 401(a) plans, to take advantage of the credit to convert to a stand-alone 401(k) or PEP. The following discussion summarizes our present understanding.

What if the Employer Already Had a SIMPLE or SEP?

In general, the credit is unavailable if the employer contributed to a plan (including employee deferrals) in the prior three years, and “plan” includes SIMPLE and SEP IRAs. But exceptions apply, and there appears to be grey area for interpretation by an employer with help from tax advisors.

Our understanding:

- The plan must be “new”

- “New” is described in section 45E(c)(2):

-

- The term “eligible employer” “…shall not include an employer if, during the 3-taxable year period immediately preceding the 1st taxable year for which the credit under this section is otherwise allowable for a qualified employer plan of the employer, the employer or any member of any controlled group including the employer (or any predecessor of either) established or maintained a qualified employer plan with respect to which contributions were made, or benefits were accrued, for substantially the same employees as are in the [new] qualified employer plan.” [emphasis added]

- “Qualified employer plan” is a defined term used on both sides of the determination: if you are starting a new “qualified employer plan” it means you have not already established or maintained any other “qualified employer plan” UNLESS the new plan is for a different group of employees (i.e., not “substantially the same employees”) or UNLESS there were no contributions in the prior three years • “Qualified employer plan” means a qualified employer plan within the meaning of section 4972(d) (see above), which includes SEPs and SIMPLEs

- Therefore, if you have or maintain a SEP or SIMPLE or other qualified employer plan for “substantially the same employees” in the prior three years, AND if you make any contributions during that time, it would appear the credit is unavailable even if the employer did not take advantage of the credit11

- If there is wiggle room for interpretation by taxpayers and their advisors on this, it might be in the following area:

- Safe interpretation: cover substantially more people than before

- Alternate scenarios may be reasonable: for example, an employer who had a SIMPLE IRA pre-COVID, suspended contributions during COVID, had extensive employee turnover, and now has a new workforce and wants to participate in a PEP or start a 401(k) is probably unlikely to be challenged if taking the credit“Substantially the same employees.” Significant changes in covered employee population between old and new plans appear to make the credit available again.

-

Is the Credit Available for Starting a SIMPLE or SEP?

- Yes. “Qualified employer plan” includes SIMPLE and SEP IRAs.

- And since the credit is available, an employer cannot use the credit for “upgrading” from a SIMPLE or SEP to a 401(k) or PEP except under the exceptions noted above since the upgrade does not meet the definition of “new” plan

- As has been pointed out to us, there is a doubtless unintentional inequity in this interpretation: SIMPLEs and SEPs have very low employer costs associated with them, so the fact that the credit is available is not especially meaningful, and excluding employers from taking the credit when they upgrade to a 401(k) does not seem in line with Congressional intent. But this is how we currently understand the amended statute.

A Word on 403(b)s and Not-for-Profit Employers

A significant problem with the tax credit is that it does nothing to help not-for-profit employers start plans. The coverage, participation, and equity gaps that the law is specifically attempting to correct apply just as much to nonprofit employers as to for-profit employers, so perhaps lawmakers will take up this cause and fund startup credits for nonprofit employers in the future. In the meantime, no credits are available to tax-exempt employers.

Explanation: SECURE 2.0 amends the existing IRC Section 45E business tax credit, which is a “nonrefundable” credit against taxes owed or paid, dollar-for-dollar. A “refundable” credit is one that is paid to the taxpayer via a tax return even if there is no tax liability. Creating credits for nonprofits would require a new type of credit, not a business tax credit.

Tax Credit for Auto-Enrollment

The credit for adding an Eligible Automatic Contribution Arrangement (EACA) under IRC Section 45T remains unchanged.

We see nothing in the statute to suggest that the credit is not available to employers who include an EACA/QACA just because doing so is now mandatory for new plans under SECURE 2.0 Section 101. This is important: all new plans established from today forward must have an EACA or QACA starting in 2025, which means all new plans qualifying for the startup credits also qualify for the additional $500 credit for including auto-enrollment if they go ahead and include that provision from the start. The industry chatter so far is that this is the way to go: include auto-enroll from day one in all startups to avoid having to add it in the near future.

About GPS and PRI

Group Plan Systems, LLC (GPS) is an independent fiduciary and consultant specializing in group retirement programs. GPS serves as a pooled plan provider, named fiduciary, and plan administrator under ERISA Sections 3(44), 402(a), and 3(16), meaning we stand in the shoes of a retirement plan sponsor and execute their duties as a professional operational fiduciary. We are also available to help financial professionals looking to learn more about developing and operating group plan programs.

For more information about GPS, please contact us at info@groupplansystems.com.

Pension Resource Institute (PRI) delivers strategic consulting, compliance, training and technology-based solutions to banks, broker-dealers, and registered investment advisers serving retirement investors. PRI’s RetirementAdvantage platform provides members with web-based access to a suite of model forms, including, but not limited to, Investment Fiduciary and Retirement Plan Consulting Agreements for ERISA 3(21) and 3(38) services, and ADV supplements for plan- and participant- level services, retirement-centric compliance procedures and disclosures for IRAs and IRA rollovers.

For more information about PRI, please contact us at info@pension-resources.com.

Any opinions or analysis are intended to be used solely for educational purposes and should not be construed as tax or legal advice, are not to be acted on as such, and are subject to change without notice. Neither Group Plan Systems, LLC nor Pension Resource Institute, LLC provides legal or tax advice.

1 The SECURE 2.0 Act of 2022, Division T of the Consolidated Appropriations Act, 2023.

2 From the user-friendly version of the United States Code maintained by the Legal Information Institute of Cornel Law School at https://www.law.cornell.edu/uscode/text/26/45E.

3 The general business tax credit, which includes the small employer pension plan startup cost credit among over three dozen other business tax credits.

4 Be careful: “qualified employer plan” is a defined term within this section of the Code and means something different than “qualified plan” (see footnote 6).

5 IRC Section 403(a) is confusing and can mostly be ignored in this context (and most contexts): the simplified version is that it just refers to 401(a) plans funded solely by annuities. 403(a) has nothing to do with 403(b).

6 IRC Section 401(a) refers broadly to the qualification requirements for profit-sharing, 401(k), money purchase, target benefit, and defined benefit plans, but not 403(b), 457(b), SIMPLE-IRA, and SEP-IRA plans. Strict usage of the term “qualified plan” among pension geeks refers only to 401(a) plans since that is the Treasury Department convention.

7 We find this section confusing: the simple version is you can’t take the credit AND a deduction for the expenses. The tricky part: can you claim the credit and still deduct SOME expenses that were not covered by the credit; if so, how much? This will require clarification from a tax professional and/or the IRS.

8 100 or fewer employees with $5,000+ of compensation in the prior year.

9 The two-year grace period, which is applied on a more limited basis here, for the contribution credit, than for the basic startup credit.

10 This paragraph makes our heads hurt. The simplest approach is that an employer needs to meet the 100 employees/$5,000+ rule every year they claim the contribution credit, with the caveat that there are exceptions that may be explored by the employer’s accountant. Do not make the mistake of thinking that this paragraph applies to anything but the determination of employer eligibility under the contribution credit (not the basic startup credit).

11 Consult a tax professional for options, which could include filing an amended return if the cost/benefit is favorable enough.

Copyright © 2023 Group Plan Systems, LLC and Pension Resource Institute, LLC, All Rights Reserved